The fate of farmers in India lies between monsoons and the markets

Date : 18/05/2024

(This is Part 1 of the series on the new Farm Bills. Access Part 2 here and Part 3 here)

India’s success in agriculture spans over crop and livestock production through green revolution technologies emphasizing on stability and adaptability over heterogeneous agroclimatic zones. While the productivity rise has been achieved, it has not necessarily led to corresponding rise in the farm incomes. One of the constraints widely recognized by farmers, researchers and policy makers in this regard is the increasing market imperfections and market inefficiencies in the existing agricultural markets. Market imperfections refer to the presence of a few buyers facing a large number of sellers characterising an oligopsony market. Market inefficiencies refer to lack of infrastructure for marketing inter alia proper roads, storage facilities, weighment facilities, grading facilities, undercover sales, illegal deductions from the payment to farmers by middleman, improper weighment, interlocked market of credit with produce market which exacerbate inefficiencies. The distress sale further forces farmers to sell their produce at the in-competitive price resulting in low incomes.

According to the FAO1, the performance of a marketing system can be assessed using the measures such as (1) farmer's share of the retail price paid by the end user or consumer (2) gross marketing margin or farm-retail price spread, and (3) proportion of consumer's income which must be spent on food. In India, farmers are receiving less than 50% of the consumer Rupee which constrains enhancing their incomes due to widening market margins and marketing costs due to presence of superfluous middlemen.

Recognizing the above agricultural market inefficiencies and imperfections, the Lok Sabha recently passed a new Act providing freedom for farmers to market their produce beyond the limits of APMC market yards, an Ordinance concerning contract farming providing price insurance and amendment to The Essential Commodities Act to enable entrepreneurs to stock produce for further processing, exports and trade purposes, to realize scale economies in marketing. In a series of articles, I would be reviewing each of these new laws and analysing the implications to farmers.

The Farmers' Produce Trade and Commerce (Promotion and Facilitation) Act, 2020

The intent of this new Act is to provide freedom for sellers and buyers to exercise freedom of choice in marketing farm produce to facilitate formation of competitive prices through alternative trading channels to promote efficient, transparent and barrier-free movement and commerce of farmers’ produce anywhere in the country as also provide a facilitative framework for electronic trading. In the Agricultural Produce Market Committees (APMC) only a limited number of traders operate leading to Oligopsony market, where there are a very few buyers to whom a large number of sellers (farmers) have to sell. Further the merchants, traders and/or commission agents form informal cartels in order to reduce the opportunity for competitive prices for the produce of farmers. According to the APMC act 1965 (of different states), farmers have to sell their produce only to the licensed traders of APMCs and receive whatever price settled and are restricted from selling their produce to anyone else outside APMCs. In addition, other than APMC licensed merchants, no one can purchase produce from farmers according to the APMC Act. Thus, the farmers could not sell their produce at farm gates, premises of factories, warehouses, silos, cold storages and also could not sell to persons, companies or cooperatives within or outside the state.

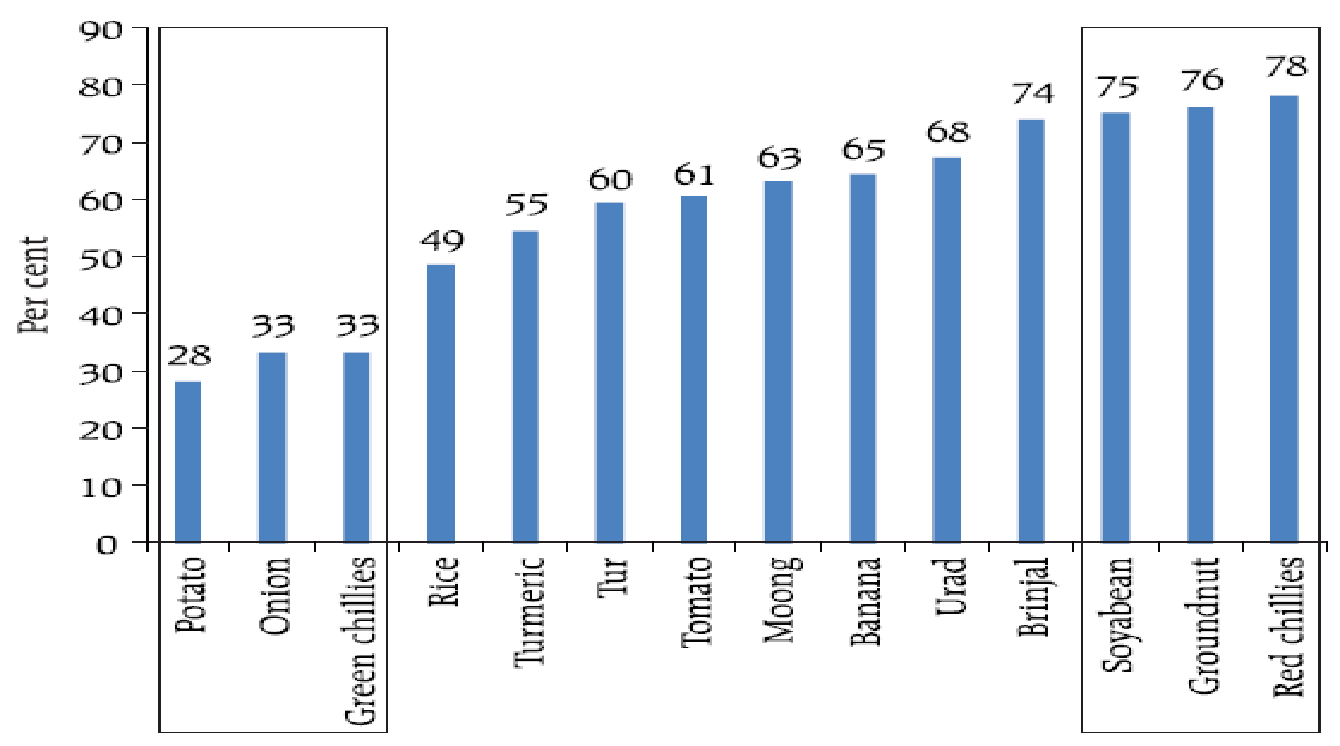

Farmer’s share in consumer Rupee

The fate of farmers in India lies between the monsoons (natural) and the markets (man-made) factors both of which have been hostile. As agricultural commodities in general and food produce in particular are characterised by relatively inelastic demand and relatively inelastic supply, they impose rigidity in farming and marketing. Therefore, a farmer is a price taker in agriculture, compared with an entrepreneur in industry or service sector who is a price maker facing relatively elastic demand. Provision of irrigation facilities, crop insurance, the vagaries in weather are addressed to some extent. However, agricultural markets have continued to be inefficient and imperfect even after 60 years of existence, due to restrictions in regulated markets on the one hand and continued exploitation by the middleman on the other. With rice being the most traded, farmers are receiving less than 50% of consumer rupee. Thus, APMCs have not been able to attract more than 50% of marketed surplus (Fig 1).

Fig 1: Farmer’s share in consumer rupee in different crops

Source: Bhoi, B.B., Sujata Kundu, Vimal Kishore and Suganti, D, Supply chain dynamics and food inflation in India, RBI Bulletin, Oct 2019, pp. 95-111.

The prima facie indicators of market inefficiency and market imperfection are the existence of a few buyers to whom a large number of sellers have to sell their produce in an Oligopsony market. These markets are not competitive (1) due to oligopsonic competition among a few traders who often form cartels resulting in collusion fail to offer competitive prices and therefore, farmers fail to receive remunerative price on the one hand, receiving a miniscule share of the consumer Rupee (2) due to existence of a large number of superfluous middleman garnering their margins at every level increasing the marketing costs and margins. For instance, if a commodity costs Rs. 6 per unit at retail level, the wholesaler would have received 67% of the retail price, the secondary commission agent 50% of the retail price, trader 37% of the retail price, primary commission agent 30 % of the retail price, consolidator 22 % of the retail price and the farmer who produced the crop with his sweat and blood, a mere 17% of the retail price (Fig 2).

Fig 2: Superfluous middleman masking the agricultural markets

Source: Source: Final Report of Committee of State Ministers, In-charge of Agriculture Marketing to Promote reforms, Ministry of Agriculture, Department of Agriculture and Co-operation, Government of India, 2013.

The existence of superfluous middleman not only increases the marketing cost on the one hand, also reduces the producer’s share in consumer rupee on the other (Fig 3)

Fig 3: Schematic representation of commodity value chain in India and US

Source: Final Report of Committee of State Ministers, In-charge of Agriculture Marketing to Promote reforms, Ministry of Agriculture, Department of Agriculture and Co-operation, Government of India, 2013.

Support to agriculture since liberalization is reducing

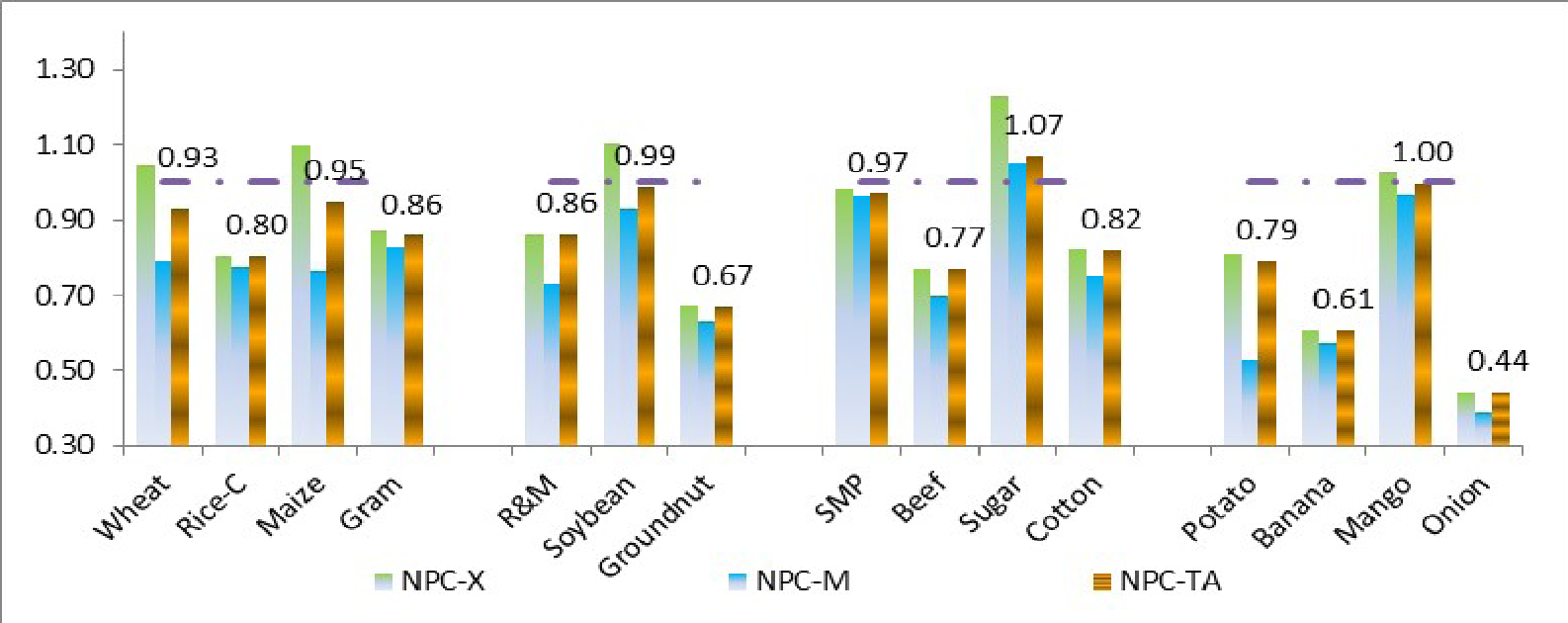

After economic liberalization in 1991, India entered WTO in 1995, and free trade was expected to result in competition and efficiency. The effects of WTO have been in rationalizing and reducing support to Agriculture and India began restricting the subsidies to less than 10 percent of the gross value of agricultural output. Currently, the support to agriculture in India is negative being - 4.97 percent or minus 5 percent of the gross farm receipts in 2019. However, liberalization did not result in increased competition in the APMC regulated markets because of rigid rules preventing competition in APMCs as farmers had to sell their produce only to the APMC merchants where price formation was not competitive. Prices were rigid due to informal cartels. The overall Nominal Protection Coefficient2 in agriculture in 2019 was 0.87 which implied that Indian farmer on an average could realize 13 percent higher price in the international market if s/he exported. Looking at the average NPC figures for these commodities (Figure 63), we see that only one commodity (sugar) had an average NPC greater than one. Mangoes had an NPC exactly equal to one. For three more commodities, maize, soybean and SMP, the 10 year average NPC TA was quite close to one. Wheat, with an average NPC of 0.93 was only lightly taxed by trade policy. Of the other key staples, rice (common) was taxed by 20 percent and potatoes by 21 percent. Buffalo meat was taxed an average of 23 percent, while groundnuts were taxed by 33 percent. Bananas were taxed by 39 percent on average, and onions by a staggering 56 percent. These results, of general taxation of the agricultural sector, are much closer to the picture for developing countries found in Krueger, Schiff and Valdes (1988) than the picture of generally positive support found in Anderson (2008).

Fig 4: Ten year average adjusted Nominal Protection Coefficients with X = Exportable hypothesis, M = Importable hypothesis, TA = Trade adjusted hypothesis;

Source: Shweta Saini and Ashok Gulati, Price Distortions in Indian Agriculture, 2017 International Bank for Reconstruction and Development / The World Bank, Washington DC 20433

Thus, the implication of low NPC for these 15 agricultural commodities for our farmers is that they can realize higher prices in the international market than in the domestic market by exporting. And to enable this, our domestic markets need to be competitive. The new Act will liberate the farmer from the clutches of APMC middleman and can choose to sell produce at any place to any buyer of his/her choice and can make use of opportunity to be a price maker from a price taker through competition.

In the next piece, I will talk about the Minimum Support Price and other allied issues.

Picture sourced from Pixabay

M G Chandrakanth is Director (Retired), Institute for Social and Economic Change, and Professor (Retd), Dept of Agricultural Economics, University of Agricultural Sciences, Bengaluru

Footnotes

1) http://www.fao.org/3/w3240e/w3240e12.htm

2) NPCi = Pd i / Pw I, NPCi : Nominal Protection coefficient of commodity I; Pd i = domestic price of commodity I; Pw i = World reference price (border price equivalent) of commodity i, adjusted for transportation, handling and marketing expenses. If NPC <1, domestic prices are < international prices and our produce is internationally competitive.

Tags :

Note: Your email address will not be displayed with the comment.

.png)